NEW HANOVER COUNTY — On Monday morning, County Commissioners discussed options for investing and managing $1.25 billion in proceeds from the sale of the New Hanover Regional Medical Center if it is approved next month.

The proposed plan would see an 11-member board controlling the $1.25 billion. Five of these members, a minority, would be appointed by county commissioners; six would be appointed by a new hospital board set up by Novant (provided the county completes the sale of NHRMC).

In theory, the money could serve as an enduring principal with investment returns providing millions of dollars annually for community projects. A super-majority of the board would be required to make substantial changes to the foundation’s mission or investment management.

According to County Manager Chris Coudriet, the reason for the board structure is twofold. First, philosophically, the minority share of the board appointments is intended to remove potential politicization of the community foundation board. Second, legally, the minority share of the appointments is intended to prevent the community foundation from falling under North Carolina laws regulating how public bodies can invest money.

Commissioner Pat Kusek recently asked county staff to map out the potential investment revenue generated at different interest rates to show how much of a difference that might make.

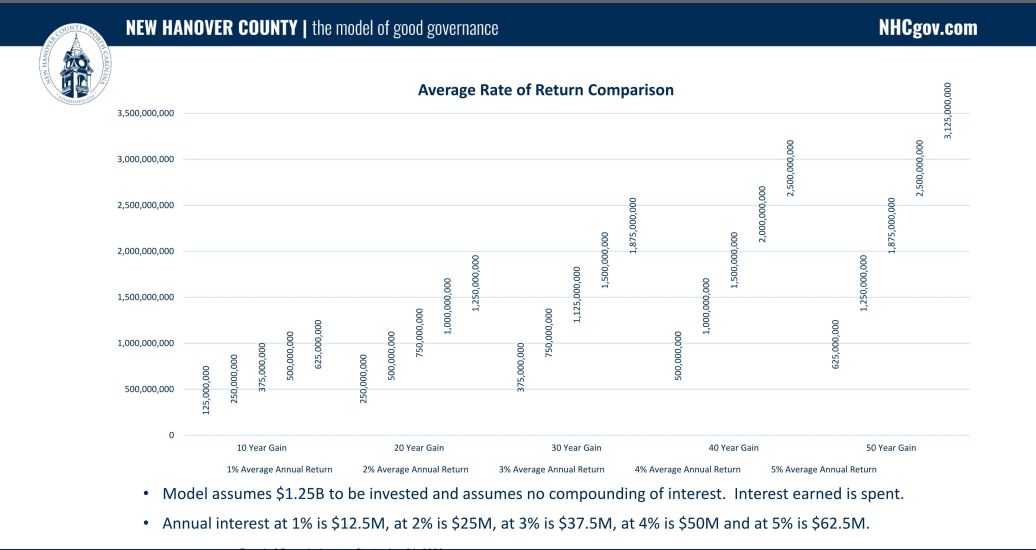

On Monday, County Finance Director Lisa Wurtzbacher gave commissioners a presentation showing a 50-year timeline for return on investment at various rates, from $12.5 million annually at 1% to $62.5 million at 5%. After 50 years, that added up to a difference of $2.5 billion between the highest and lowest interest rates.

Wurtzbacher noted that the county’s investment return rate averaged 2.18%, with no individual instrument earning more than 2.8%. The implication was that the county’s finances are a representative rate of return on government investment — and that private investment could generate more money. As Kusek pointed out, that’s money that would be invested in the community.

Wurtzbacher confirmed to Commissioner Woody White that the rate comparison did not include compounded interest but that, in practice, it certainly could.

While Kusek effectively asked the county to look at potential reward, Commissioner Rob Zapple asked about the flip-side of more aggressive investment — namely, potential risk. Zapple asked, by way of example, if the county had factored in market recessions.

Wurtzbacher noted that the estimates did not factor in recessions or market booms.

Zapple also argued that he felt that the community foundation board would fall “squarely under” state law, regardless of whether the county commissioners appointed a minority or majority. Zapple said it was his interpretation that §159-30(8) would under the oversight of the Local Government Commission (LGC). This would, in effect, negate the benefit of surrendering majority control of the community board by the county commissioners, because the LGC would likely check efforts to make riskier, more financially rewarding investments.